For decades, the traditional 60/40 portfolio was considered the foundation of long-term investing. Allocate 60% to stocks for growth and 40% to bonds for income and stability, rebalance occasionally, and let compounding work over time.

It was simple, easy to understand, and for many years it worked well.

But investing isn’t about following the same formula forever. Markets change. Interest rates change. Inflation changes. Your portfolio should adapt as well.

Over the past decade, one question has become increasingly important: Is a 40% bond allocation still the best default strategy?

I’ve wrestled with this question over time. My style of investing is a mix of growth and value on the equities side, with an allocation to bonds, alternatives, and a small amount of cash.

I used to favor something like a 65%/35% split. Over the past few years, it’s more like 70%-75% equities/alternatives and 25%-30% bonds, with a good portion of the portfolio using return stacking methodology.

More market exposure increases volatility, but it also provides for more efficient investing with better risk-adjusted returns.

Even for retired clients.

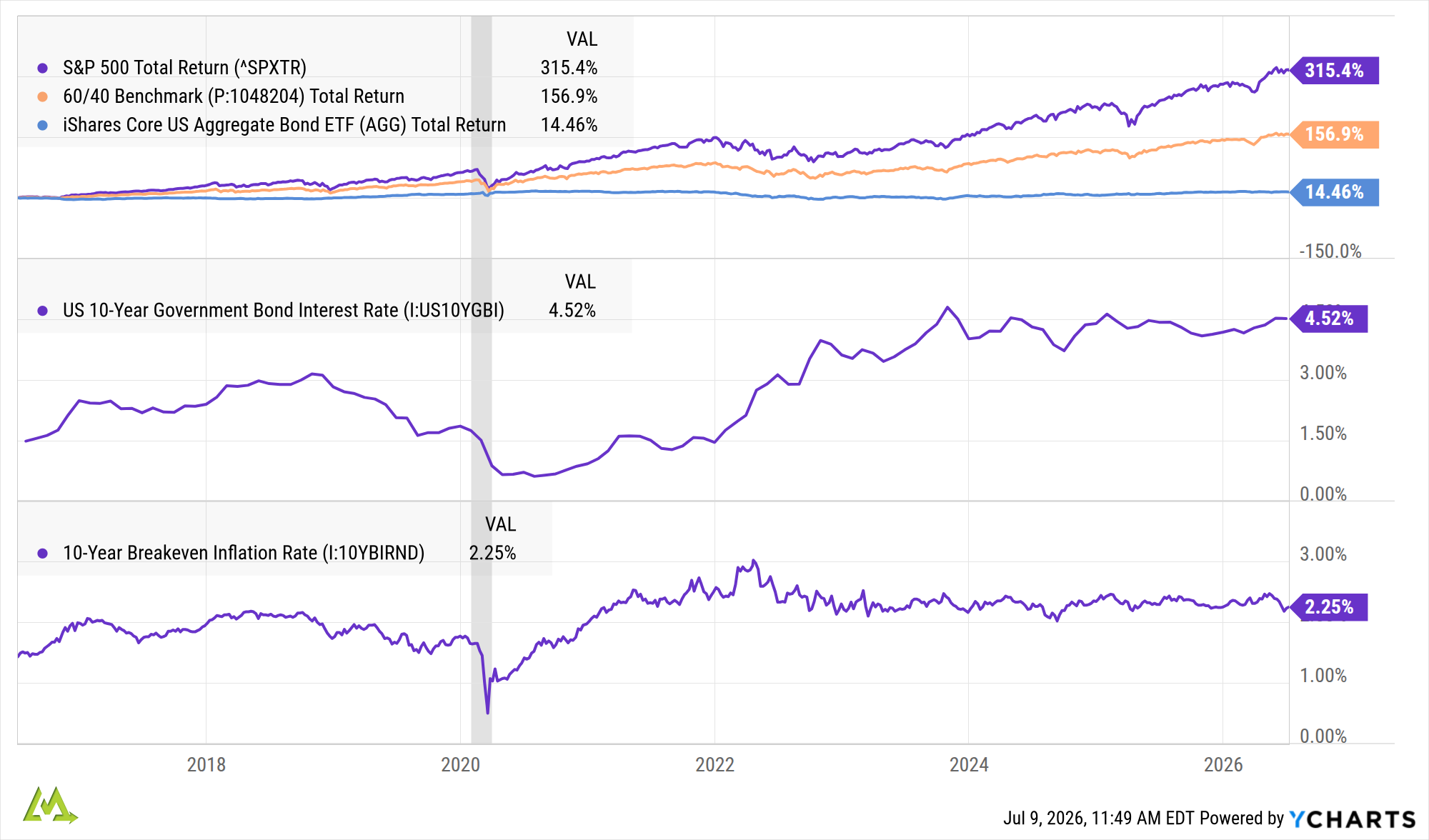

Over the last ten years, the S&P 500 Total Return Index gained roughly 315%. A traditional 60/40 portfolio—60% invested in the S&P 500 and 40% in the Bloomberg U.S. Aggregate Bond Index—returned approximately 157%.

Meanwhile, the bond portion of the portfolio, represented by the iShares Core U.S. Aggregate Bond ETF (AGG), gained only about 14.5%.

That’s a significant performance gap.

The bond allocation didn’t simply reduce volatility. It also meaningfully reduced long-term returns. More importantly, this wasn’t caused by one bad year. It was the result of a decade-long shift in interest rates and inflation.

From 2015 through 2019, bonds generally behaved as expected. They produced modest income, helped smooth portfolio volatility, and often moved differently than stocks during periods of market stress. They weren’t exciting, but they provided valuable diversification.

The Federal Reserve lowered interest rates to nearly zero in response to COVID-19. Inflation-adjusted, or real, yields fell into negative territory, meaning investors were accepting returns that failed to keep pace with inflation. Bond prices initially benefited from falling rates, but future return potential became increasingly limited.

As inflation began to increase through 2021, the Fed called it “transitory” and left rates near zero. Everything changed again in 2022.

As inflation accelerated through the first half of the year, the Federal Reserve implemented one of the fastest interest rate hiking cycles in decades. Bond prices fell sharply as rates increased, producing one of the worst years in the history of the broad bond market.

Even more surprising, bonds declined alongside stocks.

For generations, investors relied on bonds to help offset stock market losses. In 2022, that relationship largely broke down. The diversification many investors expected simply wasn’t there when they needed it most.

Today, the environment looks different.

Interest rates are significantly higher, and real yields have returned to positive territory. That’s actually good news for future bond investors because higher starting yields have historically led to better long-term returns.

Bonds continue to play an important role for many retirees, conservative investors, and anyone with shorter-term spending needs. They can provide liquidity, income, and reduce overall portfolio volatility.

The better question is whether 40% in traditional investment-grade bonds should still be the default recommendation for everyone. My argument is for most people there’s not much sense in allocating more than a third of the portfolio to an area generating lower real returns over the past decade.

But, we have to acknowledge that financial planning isn’t about applying the same allocation to every investor. It’s about building a portfolio that aligns with your goals, tax situation, cash flow needs, time horizon, and tolerance for risk.

Depending on those factors, today’s portfolios may benefit from incorporating shorter-duration fixed income, managed futures, alternative income strategies, buffered ETFs, or other investments designed to provide diversification beyond traditional bonds.

The goal isn’t to chase performance. It’s to build a portfolio that’s resilient across a variety of market environments. The past decade has reminded us that every investment strategy deserves an occasional review.

The best portfolio isn’t the one that’s been around the longest. It’s the one that’s built for the environment ahead while remaining focused on helping you achieve your financial goals.

Could your portfolio benefit from a smarter approach to investing? We can help.

Disclosures

Life Moves Wealth Management is a registered investment advisor offering advisory services in the States of Arizona and Indiana, and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. Information contained on this site should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

The information on this site is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

HYPERLINK DISCLOSURE – The information being provided is strictly as a courtesy/convenience. When you link to any of the web sites provided here, you are leaving this website and assume total responsibility and risk for use of the web sites you are visiting. We make no representation as to the completeness or accuracy of information provided at these websites. Life Moves Wealth Management is not liable for any direct or indirect technical or system issues or any consequences arising out of your access to or your use of third-party technology, web sites, information and programs made available through this website. Life Moves Wealth Management does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Life Moves Wealth Management’s web site or incorporated herein, and takes no responsibility thereof.

Author: Dale Shafer II, CFP®, CBEC®, APMA®

This website uses cookies to make sure you get the best experience on our website. You can find more information under the Privacy Policy.